About This Card

The IDFC FIRST Hello Cashback Credit Card is an FD-backed card offering up to 5% cashback on online spends, ideal for everyday users in India seeking easy approval without income proof. Launched recently, it combines UPI compatibility, interest-earning FDs, and rewards up to ₹18,000 annually, making it popular for building credit history.

Join Our Community Channels

Save Upto Rs.10,000 Per month with exclusive offers and deals. Get instant alerts!

As of now, the best card in the cashback segment is only the SBI Cashbak credit card and every bank wants to beat it, but none can. IDFC’s new Hello Cashback card brings something in the market, but not as good as SBI’s Don Cashback card

Checkout Scapia Credit Card Which is Lifetime Free & Offers Flight Discounts

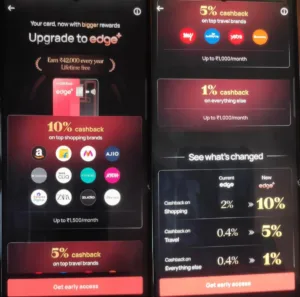

This card delivers tiered cashback on online spends: 3% up to ₹10,000 and 5% on amounts above that per statement cycle, capped at ₹1,000 for online. Additional 1% applies to UPI via IDFC app, in-store swipes, and essentials like rent, utilities, education, FASTag, insurance, and wallet loads; total cap is ₹1,500 monthly. Bonus 1% extra on hotel/flight bookings via bank app pushes travel rewards to 4-6%, while exclusions cover fuel, EMIs, ATM withdrawals, and non-IDFC UPI apps.

How To Apply For IDFC First Hello Credit Card

1. First of all, click on the link below to visit IDFC’s website to start your application.

2. Now, once you are here, fill in your basic details with OTP verified mobile number.

3. Enter Adhaar number, PAN number and other information regarding your employment

4. Verify & create an FD of the amount greater than 10,000.

5. Now you will get the virtual credit card created for you.

Additional Benefits and Privileges

Earn FD interest alongside cashback; complimentary roadside assistance (₹1,399 value, 4x/year), personal accident cover ₹2L, lost card liability ₹25,000, credit shield ₹50,000, purchase protection ₹25,000. UPI links to GPay, PhonePe, etc., but 1% cashback only via IDFC app; first 24h limit ₹5,000 post-PIN setup. Cashback credits post-payment due date if minimum due paid, viewable in statements.

Pros, Cons, and User Insights

Pros include no-income approval, high online cashback, UPI ease, and dual FD benefits for homemakers/students building credit. Cons: cashback caps, FD lock-in, limited to IDFC app for max UPI rewards, new launch with sparse 2026 reviews (positive early buzz on forums). Early users note 4-6% effective rates on select spends suit moderate spenders; compare favorably to other FD cards for rewards but check personal FD rates

Frequently Asked Questions

How does the cashback work? +

Get 3% cashback on first ₹10,000 online spends, 5% thereafter (up to ₹1,000); additional 1% on UPI/offline/essentials, with an overall ₹1,500 monthly cap. Cashback is credited after you pay at least the minimum due on time.

Is income proof required? +

No income proof is required because this is an FD-backed card. You simply create a fixed deposit of at least ₹10,000 during application, and your credit limit is typically set equal to the FD amount.

Can the annual fee be waived? +

Yes, the annual fee of ₹1,000 plus GST from the second year can be partially waived at 50% for annual spends between ₹1 lakh and ₹2 lakh, and fully waived for annual spends above ₹2 lakh, excluding cash advances and EMIs.

What happens to my FD when I take this card? +

Your FD is placed under lien and cannot be prematurely withdrawn while the card is active, but it continues to earn interest and can be released once dues are cleared and the card or lien is closed.

Is it good for UPI payments? +

Yes, you earn 1% cashback on UPI spends when the card is linked and used via the IDFC FIRST Bank app, subject to the overall monthly cashback cap, while standard UPI usage on other apps may not earn the same benefit.

Do I get cashback on rent and bill payments? +

Yes, eligible rent payments, utility bills, education payments, government services, FASTag reloads, insurance premiums, and select wallet loads usually earn 1% cashback, subject to exclusions and overall caps.

Are there categories where cashback is not given? +

Yes, certain transactions like fuel spends beyond surcharge waiver, cash withdrawals, EMI conversions, and specific wallet or quasi-cash transactions typically do not earn cashback as per the card’s terms.

When is the cashback credited to my account? +

Cashback is usually computed on the statement cycle and credited after the payment due date, provided you have paid at least the minimum amount due and your card account is in good standing.

Is there any cap on monthly cashback? +

Yes, online spends can earn up to ₹1,000 cashback per statement cycle, and the total cashback, including offline and UPI, is capped at around ₹1,500 per month as per the bank’s structure.

Can I increase my credit limit later? +

Your credit limit is linked to your FD value, so you can usually increase it by creating or enhancing the FD under lien; in some cases, the bank may also offer limit enhancements based on usage and repayment.

Is this card suitable for building credit history? +

Yes, this FD-backed card is ideal for first-time users, students, and homemakers because on-time repayments are reported to credit bureaus, helping build or improve your credit score over time.

Can I convert big purchases into EMIs? +

Most large eligible transactions can be converted into EMIs through the app or customer care, though such EMI transactions typically do not earn cashback and may attract separate interest or processing charges.

Do I get lounge access with this card? +

The Hello Cashback Card primarily focuses on cashback and FD-backed approval, so airport lounge access benefits, if any, may be limited or available only through periodic offers rather than as a core feature.

What insurance benefits are included? +

The card usually comes with complimentary covers such as personal accident insurance, purchase protection for eligible items bought on the card, and a credit shield benefit for specified events, subject to policy terms.

Is there any fuel surcharge waiver? +

Yes, there is typically a 1% fuel surcharge waiver on eligible fuel transactions at specified outlets, subject to a maximum monthly cap, although such fuel spends may not earn regular cashback.

How quickly can I start using the card after approval? +

You receive a virtual card almost instantly after approval and FD creation, which can be used for online transactions and UPI linking, while the physical card is dispatched within a few working days.

Can I use this card for international transactions? +

The card is generally enabled for domestic usage by default, and international usage may be controlled via the app; foreign currency transactions will attract applicable forex mark-up and may not get special cashback.

What happens if I miss a payment? +

If you miss paying at least the minimum due by the due date, late payment charges and interest will apply, your cashback for that cycle may not be credited, and prolonged non-payment can lead to FD lien invocation.

Can the bank liquidate my FD if I default? +

In case of serious or prolonged default, the bank has the right to adjust outstanding dues against the FD under lien, which may result in partial or full liquidation of the fixed deposit to recover the pending amount.

Is video KYC mandatory for this card? +

Yes, for most digital applications, completing video KYC is mandatory to activate the card and FD, unless you complete full in-person KYC at a branch, ensuring regulatory compliance and seamless onboarding.

Can I close the card without closing my FD? +

If your FD is specifically created as security for this card, the lien is tied to the card, so closing the card generally requires clearing dues and then removing the lien, after which you can decide to continue or break the FD.

Is this card better than a normal unsecured card? +

For users with no or low credit scores, this FD-backed card can be more accessible and still offer strong cashback, while those with established credit and higher income might find premium unsecured cards more rewarding overall.

What is the annual fee for IDFC FIRST Hello Cashback Credit Card? +

The annual fee for IDFC FIRST Hello Cashback Credit Card is ₹1,000. Some cards may waive the annual fee based on spending criteria or for the first year.

What welcome bonus do I get with IDFC FIRST Hello Cashback Credit Card? +

New IDFC FIRST Hello Cashback Credit Card cardholders can earn Up to ₹500 cashback on first transaction. This welcome offer is typically available for a limited time and subject to meeting minimum spending requirements.

How does the Cashback system work with IDFC FIRST Hello Cashback Credit Card? +

IDFC FIRST Hello Cashback Credit Card offers Cashback as rewards. The conversion rate is Direct cashback credited to statement. You can earn Up to 5% on online spends on various categories.

What are the eligibility criteria for IDFC FIRST Hello Cashback Credit Card? +

To be eligible for IDFC FIRST Hello Cashback Credit Card, you need a minimum income of None required (FD-backed). Additional criteria may include age requirements, credit score, and employment status. Contact for complete eligibility details.

How long does it take to get IDFC FIRST Hello Cashback Credit Card approved? +

The typical processing time for IDFC FIRST Hello Cashback Credit Card is Instant approval with video KYC. Processing times may vary based on document verification and credit assessment. You may receive instant approval for pre-approved applications.

How can I apply for IDFC FIRST Hello Cashback Credit Card? +

You can apply for IDFC FIRST Hello Cashback Credit Card online through our secure application process. The application is quick and convenient, requiring basic personal and financial information.

Comments